Our strategic goal in supporting SMEs consists in providing a better access to long money sources for those SMEs that facilitate a more competitive economy, create new highly productive jobs and work towards regional sustainability.

Vnesheconombank plays the leading part in the implementation of the national SME development policy. Since 2007, we have been successfully carrying out the Programme for Financial Support to SME operated by our subsidiary, SME Bank. Since 2013, SME Bank has also been putting in place a mechanism for guarantee-based support to medium-sized enterprises that are not involved in the production and processing of mineral resources.

Apart from SME Bank, the development of the SME segment is also strongly supported by other entities of the Group, first of all by VEB-Leasing that promotes leasing services in the SME segment, and Globexbank and Sviaz-Bank that are running their own SME lending programmes.

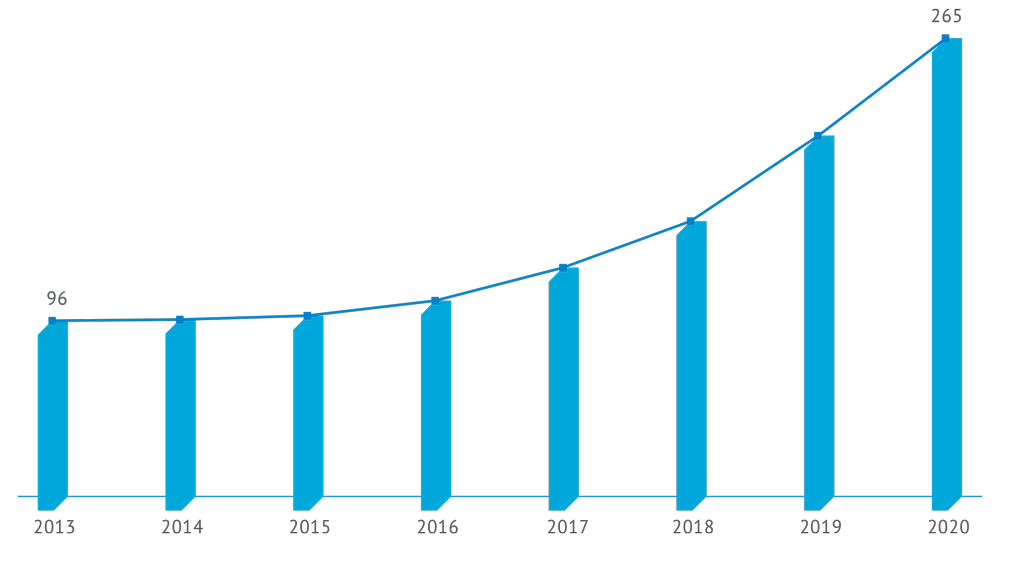

Vnesheconombank’s Development Strategy for 2015–2020 provides for further increase in the amount of funds allocated to SME that is planned to reach RUB 225–265 bn under the modernisation scenario by the end of 2020.

By implementing its programme for financial support to SME, Vnesheconombank is planning to achieve the following by the end of 2020:

secure up to 5.6% of the overall financing of SME forecast for late 2020 by allocating RUB 180 bn for long-term (over 3 years) support to SMEs;

provide RUB 175 bn of support to non-trading SMEs by increasing the programme’s share in the market of loans to non-trading SME to 4.5%;

create or upgrade each tenth highly productive job in the SME segment.

In 2014, the Russian Government decided to extend the maturity of its RUB 30 bn deposit of funds from the National Wealth Fund with Vnesheconombank until the end of 2027. The money was deposited to secure the resources for the implementation of the programme for financial support to SMEs. This decision will also work towards the successful achievement of the strategy’s targets.

Funds allocated to SMEs under the modernisation scenario (RUB bn)

With the Russian economy passing through such turbulent times, it is small and medium-sized businesses that are able to smooth down negative processes in the employment market, ensure social adaptation of those employees that leave large enterprises, and build new market niches and economic growth centres.

With the macroeconomic situation going downhill in 2014, the SME lending market showed a poor performance. SME input in GDP was about 20-21%, which does not exceed the post-crisis level of 2011–2013. At the same time, the number of new SMEs went down to 1.7% against 3% in 2013.

SME growth mostly slowed down due to weaker lending and tougher access to loans. Thus, in 2014, the share of loans with maturities exceeding 3 years in total loans to SME was only 11.5%, while average weighted interest rates were continuously rising, and requirements to collateral and the financial situation of borrowers growing stricter.

State of the SME Market

Loans issued to SME

7,610.59RUB bn

Outstanding debt by SME

5,116RUB bn

Distressed debt by SME

394.4RUB bn7.7% in the total SME loan portfolio

Average weighted interest rates on loans to SME

14.92%for > 1-year loans

16.09%for < 1-year loans

Performance dynamics as compared to 2013

5.6 %4-year low since 2011

0.9 %

0.7 percentage points

209 basis points year-on-year

360 basis points year-on-year

Ensuring SME growth by reducing financial and administrative costs is one of the priorities set out in the plan on Priority Measures to Ensure Sustainable Economic Development and Social Stability in 2015 approved by the Russian Government in 2015. The plan provides for doubling the maximum revenue required for business entities to be classified as SME, expanding the range of measures designed to support innovative small-sized enterprises and reducing excessive tax burden that puts a drag on SME growth.

Outcomes of the Programme for Financial Support to SMEs

The Programme for Financial Support to SME seeks to provide credit support to SMEs from key customer segments of SME Bank. According to SME Bank’s strategy for the period until 2020 approved in 2014, the bank is to re-focus on new customer segments that include SMEs operating in single-industry towns and in regions with a challenging social and economic situation, SMEs that are residents of industrial parks, and SMEs that produce goods and services for large businesses and government-sponsored companies, including as part of government procurement.

Another key focus area of SME Bank consists in long-term financing of SMEs, which has become particularly important with access by SMEs to long money shrinking. SME Bank is also responsible for building the market of instruments to refinance assets related to bank loans to SMEs. To this end, SME Bank is planning to engage in deals for securitisation and guaranteeing of loan portfolios of commercial banks operating in the SME segment.

Key development areas of the Programme for Financial Support to SMEs under SME Bank’s Strategy for 2015-2020:

long-term loans to SMEs;

loans to SMEs in industrial parks;

loans to SMEs in single-industry towns and national development priority regions (Far East, North Caucasus and Crimea).

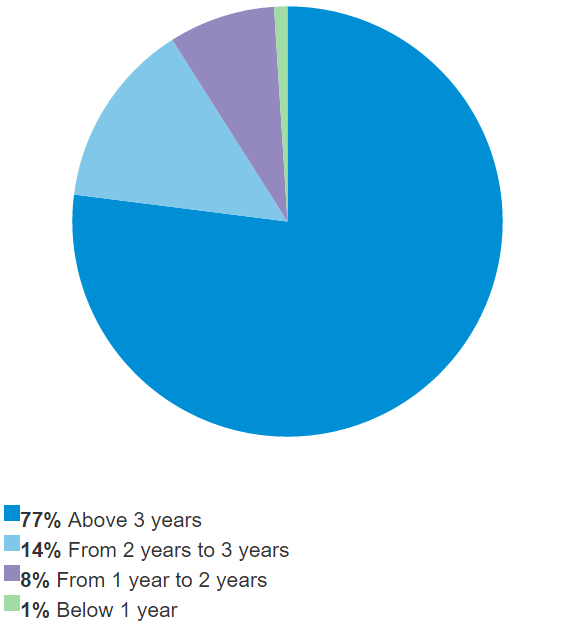

SME Bank is implementing this programme using a two-tier mechanism by financing SME via a network of partner banks and entities from a supporting infrastructure. Loans are issued to SME on a long-term basis at interest rates that are far below average market rates, which is a key criterion of the Programme’s efficiency. As at the end of 2014, the share of loans with maturities over 2 years issued under the Programme reached almost 91%, with an average weighted interest rate of 12.73% p. a.

While the market of bank loans to SMEs was collapsing, SME Bank was able to increase its SME support portfolio by 2% under the SME Programme. This was made possible, among other things, by the Programme’s focused on regions with unfavourable economic climate and an underdeveloped framework of support to SMEs. As a result, SME Bank was able to achieve a rather high share of penetration in the lending system across a large number of regions.

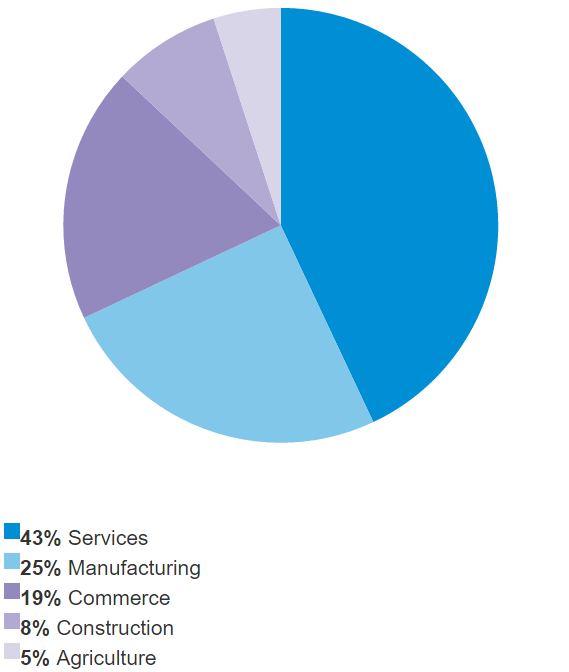

Outcomes of the Implementation of the Two-Tier Mechanism of Support to SMEs

Project: Production of Non-Ore Construction Materials

Project initiator (SME): OOO Aktivist (Republic of Tatarstan, Kazan)

Total project value: RUB 200.03 mn

SME Bank’s commitment: RUB 138.39 mn

Project goal: build a dredger — a floating engineering facility designed for underwater digging and cleaning of water bodies, dredging and extraction of non-ore building materials.

As a result of the project, the Volga and Kama River Basins will get the only local dredger that will allow producing sand and gravel mix at depths up to 30 m. The dredger will include a gravel plant to sort and enrich feedstock on the spot.

This project will supply the Republic of Tatarstan and adjacent regions with gravel and sand that are a prerequisite for any growing construction industry. High construction rates in the Republic of Tatarstan, a leader in the new housing commissioning rates in Russia, make the project extremely important.

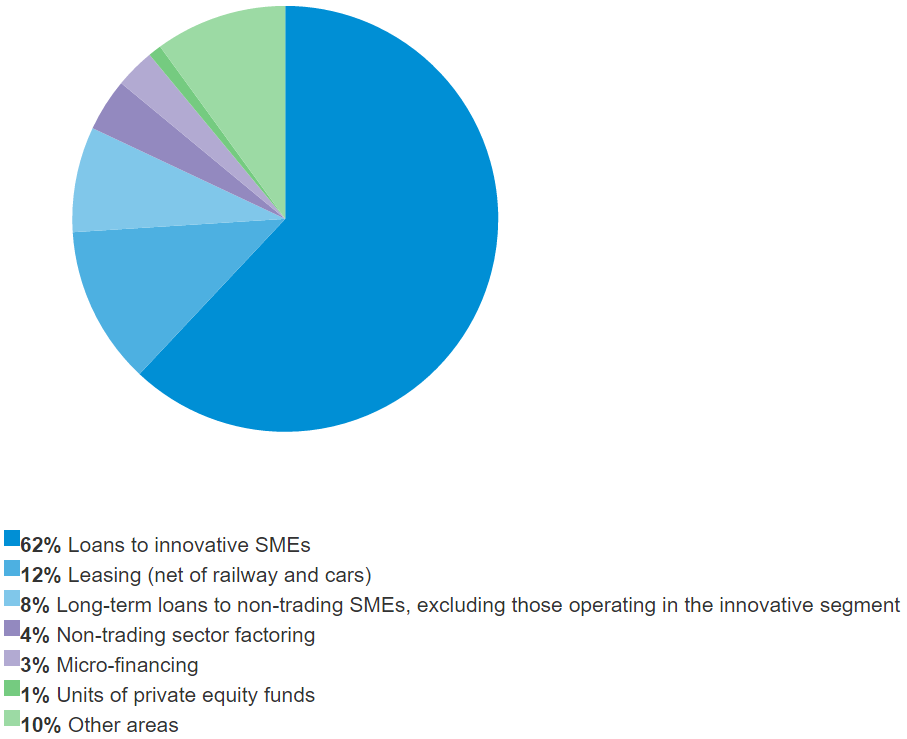

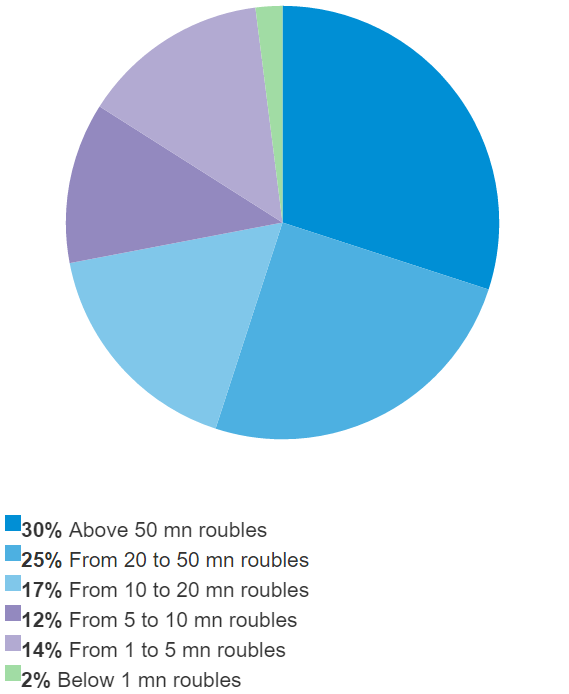

Breakdown of Distribution of Funds under the Programme for Financial Support to SMEs as at the End of 2014

Breakdown of the Programme’s funds by area of support to SME

The strategic niche — loans to innovative SMEs — accounts for the largest share in the breakdown of distribution of the Programme’s funds

Guarantee-Based Support to Medium-Sized Enterprises

In 2014, SME Bank kept implementing its guarantee-based mechanism of support to medium-sized enterprises that had been previously initiated in line with a relevant Executive Order of the Russian President. The mechanism is expanding capabilities of medium-sized enterprises in raising loans from lending institutions to support their investment projects. The support is provided to medium-sized enterprises that are unrelated to production and processing of mineral resources.

As the operator of this guarantee-based mechanism, SME Bank issues guarantees to medium-sized enterprises on their obligations to their lending banks up to 50% of the loan. Guarantee obligations of SME Bank are fully secured with a bank guarantee by Vnesheconombank, which in its turn is 50% backed with a government guarantee of the Russian Federation.

The amount of guarantees to be provided by SME Bank as part of this guarantee-based mechanism of support to medium-sized enterprises is planned to be RUB 40 bn. The mechanism is expected to help medium-sized enterprises raise up to RUB 80 bn of loan resources.

Implementation of the Guarantee-Based Mechanism of Support to Medium-Sized Enterprises

SME Bank’s commitment: a RUB 100 mn investment loan via Levoberezhniy Bank and a RUB 50 mn guarantee to secure the bank’s loan

Project goal: upgrade production facilities of the curd shop by installing a closed-type curd line and soft cheese production equipment.

As part of the project, the company will undertake a range of measures to improve the process of making its traditional dairy products and launch a new soft cheese production line. By expanding its product mix, the project initiator that operates in the SME segment will be able to reach a fundamentally new level in the market. The project will also enable the company to cut down the share of manual labour and mitigate microbiological risks by eliminating intermediate stages from the dairy production process.

Pilot Baltic Initiative

Vnesheconombank is implementing the Pilot Baltic Initiative developed under the auspices of the Russian and German Ministries of Foreign Affairs together with KfW, a German banking group. The Initiative aims to support non-trading SMEs from Russian regions adjacent to the Baltic Sea: The Kaliningrad, Leningrad, Novgorod and Pskov Regions and Saint Petersburg.

In 2012, as part of the Baltic Initiative, KfW issued a USD 110 mn 5-year loan to Vnesheconombank. In the scope of the Initiative, SME Bank is extending loans to SMEs via a network of partner banks. As at the end of 2014, the loan to KfW was partially repaid, with USD 64.8 mn of the loan facility still available to SME Bank.

In 2014, SME Bank agreed with the German party to sign a supplementary agreement that would entitle SME Bank to lend partner banks from its own resources that can be replaced with KfW funds. This step has considerably increased the number of SMEs involved in the project.

If you notice an error on this page, please let us know: